Listed real estate and short-term inflation: The European experience

By David Moreno, EPRA Indexes Manager

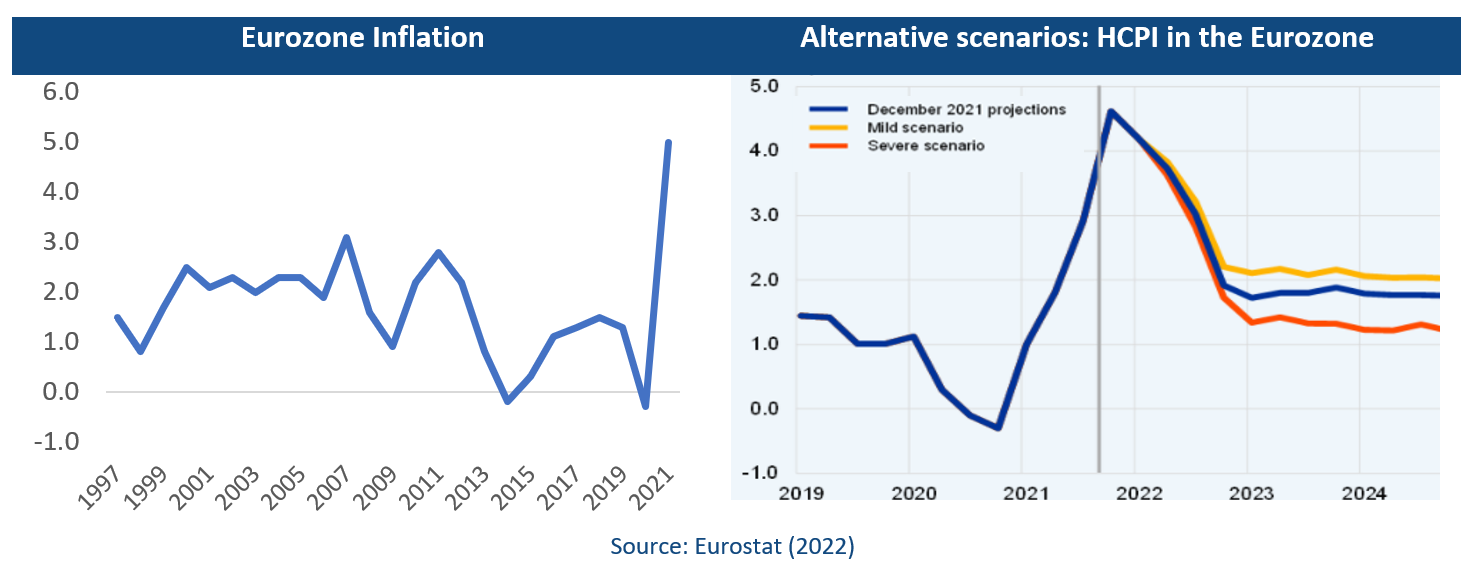

Inflation is in the eye of the storm for the majority of analysts and investors analysing expected returns and strategic asset allocations for 2022. In the Eurozone, inflation reached a record level (5.1%) in January 2022, after years of low inflation. Similar trends have been observed in Sweden, Switzerland and the UK. This can be explained by three main reasons: A quick reopening of the economy, higher energy prices and base effects (ECB, 2021). The ECB expects the inflation to gradually decrease in 2022, while the Bank of England sees inflation peaking at 7.25% around April 2022 before gradually decreasing during the rest of the year. A similar view is shared by the central banks in Sweden and Switzerland.

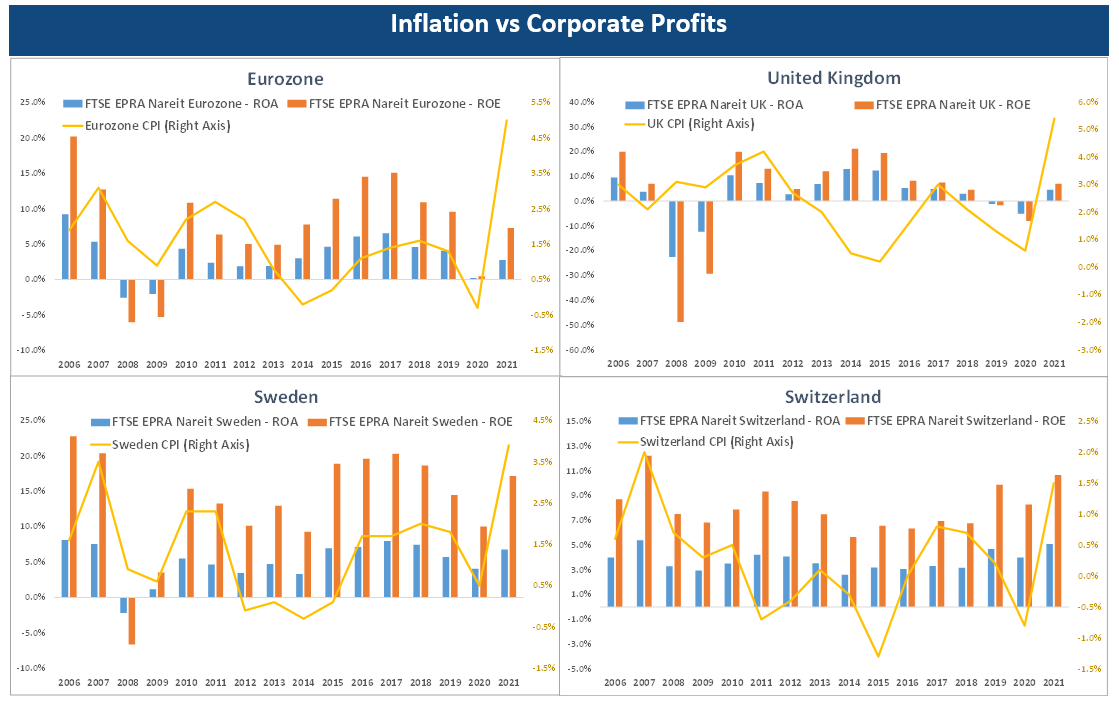

Property companies face changes on both operational revenues and expenses when inflation rises. Rental practices in Europe facilitate the integration of inflation dynamics into the companies’ revenues and support rental growth. Most of the long-term leases have Consumer Price Index-linked rent escalations, offering income protection and higher revenues, but higher inflation also means higher maintenance expenses, development costs and property acquisitions. So what is the effect of inflation on net profits and shareholders returns? There is evidence of a strong and positive correlation between corporate profits and inflation as well as shareholders’ returns and inflation.

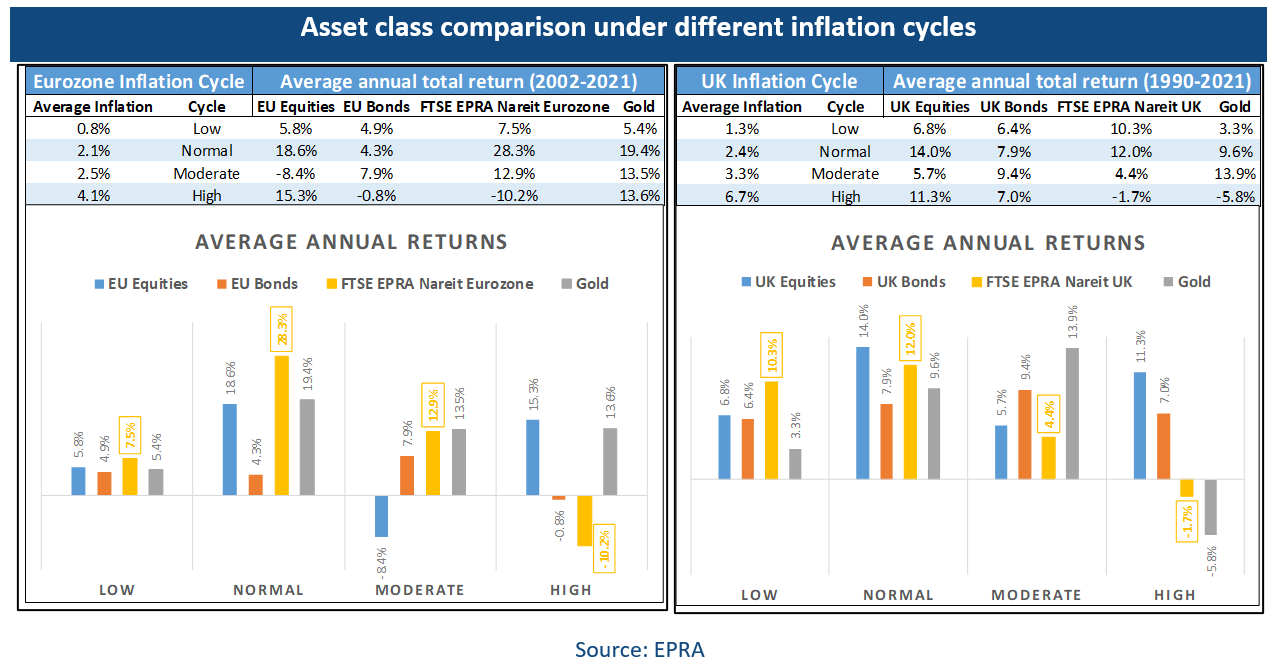

During the last 20 years, listed real estate in the Eurozone always outperformed general equity and bonds under low, normal and moderate inflation cycles. A similar case is observed in the UK for the period 1990-2021, showing a higher or similar return than general equities under the same cycles. However, under high inflation cycles (above 3.06% for the Eurozone and 5.04% for the UK1) listed real estate underperformed general equity and bonds, which is mainly the result of a combination of strong economic growth and low returns in real estate in anticipation of an economic contraction, such as the case of 1990-1991 in the UK and 2007 both in the Eurozone and the UK. EPRA estimates that a 100 bps increase in the annual inflation has a positive effect of 33 bps in the annual total return from listed real estate in Switzerland, 29 bps in the UK and 108 in Sweden. For the Eurozone, this estimation needs to be adjusted using country-specific models.

After a deep recession in 2020, last year was characterised by a clear economic recovery, forecasted by many analysts and institutions to continue on a more moderate path in 2022 and 2023. Current inflation levels are not associated with strong demand pressures but with several temporary supply disruptions. Therefore, following the market’s and central banks’ expectations, we are likely going to see a moderate inflation cycle in Europe in 2022 and 2023 that should represent a positive driver for corporate profits and returns of the listed real estate industry across the continent.

1 Moderate and High cycles are defined by the 70th and 90th percentiles respectively, 2.2% and 3.05% for the Eurozone, 2.91% and 5.04% for the UK.