By Giovanni Curatolo, EPRA Research & Index Analyst

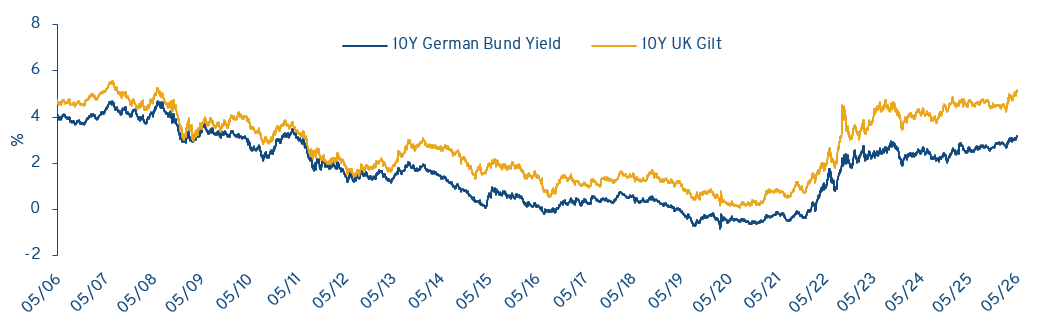

This month, long-end reference yields across major economies have reached multi-year highs. This comes as markets price in higher inflation risk and weaker growth expectations, following the prolonged conflict in the Middle East and the closure of the strategically critical Strait of Hormuz. In Europe, the 10-year German Bund yield has reached 3.2%, the highest level in the past 15 years, and in the UK, the 10-year Gilt yield has risen above 5% for the first time since July 2008 (Chart 1). Across the Atlantic, the picture is quite similar, with the 10-year Treasury yield peaking at 4.6% on May 19.

EPRA Research - Bloomberg

The implications for risky assets are theoretically straightforward. As the long end of the yield curve rises, valuations that use the 10-year government bond yield as a proxy for the risk-free rate come under pressure. However, this follows different magnitudes, with prices reacting faster than look-through asset values, and hence with public markets adjusting before private ones. When the 2021-22 rates shock happened, the sector went through a structural re-pricing, with the average discount to NAV of European listed property companies widening from 6% in August 2021 to 46% in September 2022[1]. Since then, the sector has already been pricing a higher-rate environment, with an average discount to NAV of around 25-30%. Importantly, this shift in valuation does not necessarily reflect a deterioration in underlying operating businesses.

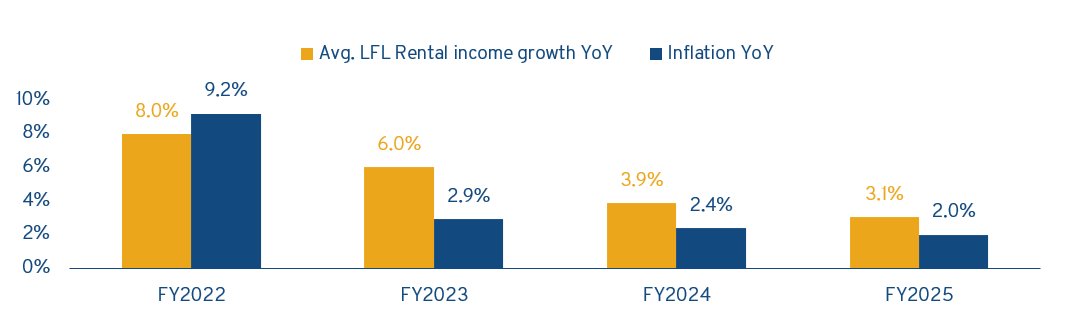

Since the 2022 rate shock, average like-for-like rental income growth has consistently outpaced inflation for most European property companies (Chart 2). This has been achieved through several channels: indexation, with rents mechanically adjusting to inflation; reversion, with expiring leases resetting to higher market rents; and active asset management, which allowed landlords to capture additional upside through refurbishment and/or repositioning of their assets.

EPRA Research[2]

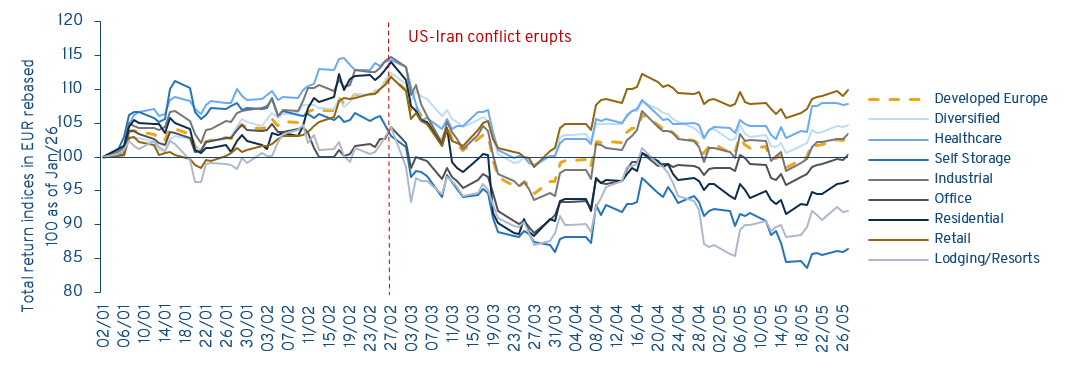

At the beginning of the year, the FTSE EPRA Nareit Developed Europe Index was delivering strong returns, with some of last year’s worst-performing sectors finally showing signs of recovery. This rebound was then interrupted by the escalation of the conflict in the Middle East (Chart 3). Since then, most sectors have declined, reversing most of the strong performance delivered in the first two months of the year.

EPRA Research

Whether the conflict is going to de-escalate this week or in a month is difficult to predict. If the situation remains static (or worsens), inflation is likely to trend even higher and central banks may be forced to raise policy rates. In that scenario, the European listed real estate sector would face pressure on two fronts: on the valuation side, due to the higher long-end yields, and on the financing one, due to the higher policy rates.

However, the sector would arguably face the shock from a structurally stronger position than in 2022. First, both underlying operations and financial positions of most European property companies are in better shape, with average rental growth consistently outpacing inflation, and net debt to EBITDA falling from around 13x in 2021 to 10.8x today. Second, the starting point for monetary policy is materially different, with major central banks reacting from a far more ‘neutral’ stance than in 2022[3], when monetary policy was looser than ever. Third, current equity valuations already reflect a higher-rate environment, following the de-rating started in 2022. If, instead, the conflict de-escalates quickly, policy rates remain somewhat stable, and long-end reference yields decline, the European listed real estate sector would be well positioned to recover, with investors benefiting from both resilient operations and potential re-rating.