Listed real estate second in institutional investment returns in Netherlands

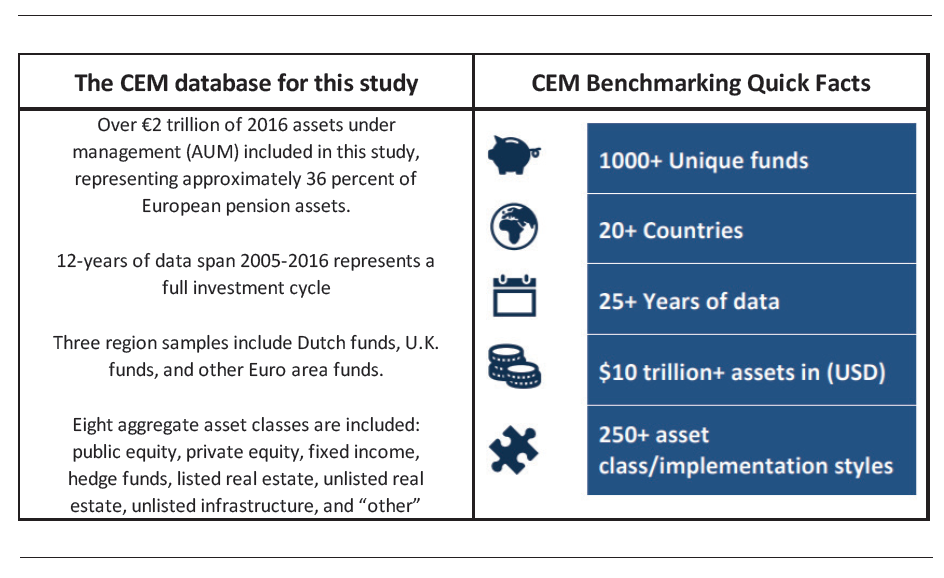

Listed real estate produced the second highest average institutional investment returns in the Netherlands (2005 – 2016) across eight major asset classes,¹ an EPRA-sponsored study by researchers CEM Benchmarking of European institutional investors has concluded. The institutions had combined assets under management (AUM) of EUR 2.6 trillion, representing 36 percent of the top 1,000 funds in Europe.

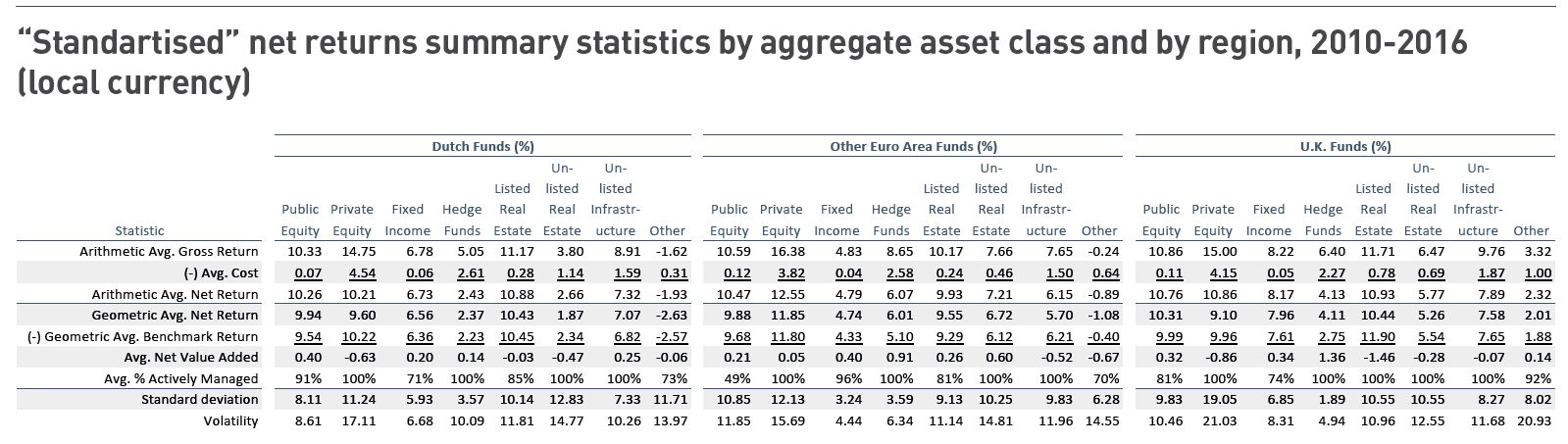

The research showed that the average annual net return for listed real estate over seven years for the Dutch institutional investors was 10.88 percent, slightly above private equity at 10.21 percent and general equities at 10.26 percent. The UK return was slightly higher at 10.93 percent, with private equity at 10.86 percent, over the same period. In the 12-years period, listed real estate average net return for Dutch funds was 9.32 percent, edging below private equity at 10.78 percent.

Listed real estate was also found to be one of the most cost-efficient asset classes in Dutch pension fund portfolios with an average investment cost of just 28 basis points. Only fixed income and public equity were found to be more cost-efficient that listed real estate, with 7 basis points and 6 basis points investment costs respectively.

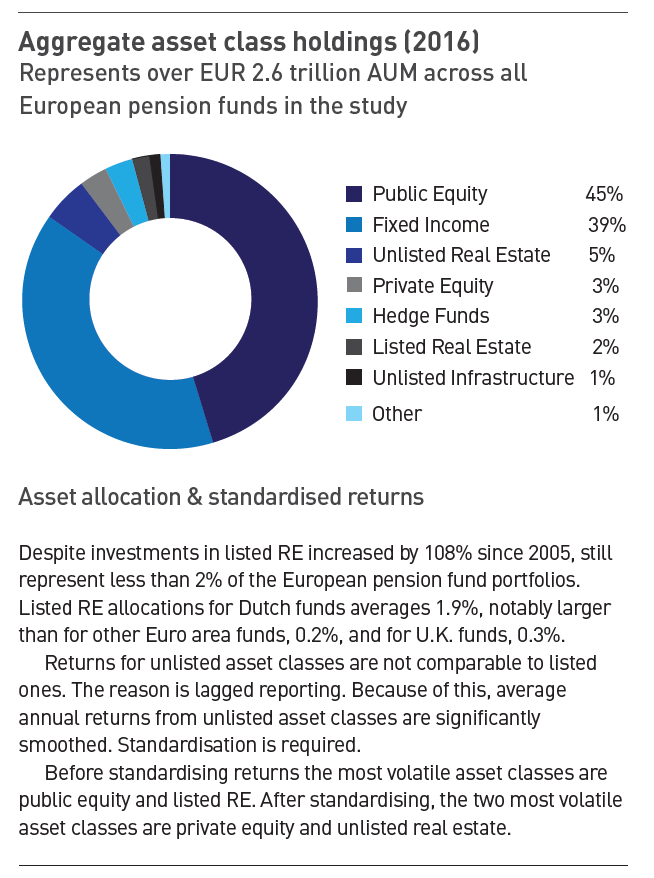

In the UK, listed real estate averaged only 0.3 percent of funds’ total AUM, but this has been increasing by a staggering +25.9 percent a year in over the research period. In contrast Dutch funds, which at 1.9 percent have the highest average institutional allocation from total AUM to listed real estate in Europe across CEM’s three sample groups (UK, NL, and other Euro area funds), show a widely diverging trend to the UK market.

“The strong returns of listed real estate demonstrate the merits of long-term institutional investor allocation to the sector independent of the general equities allotment, particularly with the risk diversification qualities this contributes to the overall portfolio,” Ali Zaidi, EPRA Director of Research & Indices, said.

“Listed real estate stocks are operating companies deriving rental income streams from the ownership and management of high-quality assets, yet at the same time providing unrivalled liquidity compared with other forms of real estate. In addition, the transparency and corporate governance of the sector gives investors’ confidence in the asset class. This research has demonstrated that the costs of listed real estate investment are a fraction of investing through funds, or holding property directly,” Dominique Moerenhout, EPRA’s CEO added.

Other key findings of the CEM Benchmarking research included:

• The average annual net investment return from listed real estate for other Euro area funds for the period 2008-2016 was 5.59 percent, compared with 11.55 percent for private equity.

• Real estate is the primary diversifier in European institutional investor portfolios, against the main fixed income and general equities asset classes. Dutch funds allocate 8.0 percent to real estate on average, split 25/75 between listed and unlisted real estate. UK and other Euro area funds allocate just over 5.0 percent to real estate on average.

• For the longest sample period where listed and unlisted real estate appear (Dutch funds 2005-2016), listed and unlisted real estate have comparable annualised volatilities (22.85 percent and 23.55 percent respectively). In other region/time samples, unlisted real estate is more volatile than listed real estate, largely due to the asset class having more idiosyncratic risk.

• Gross of investment costs, private equity was the best performing asset class overall, but also the most expensive with investment costs of 452 basis points (Dutch funds), 382 basis points (Euro area funds), and 415 basis points (UK funds). Net of investment costs, private equity returns remained the highest of all asset classes with the exception of listed real estate in the UK.

• Direct comparisons between listed and unlisted real estate in each region group / sample period did not show evidence of a liquidity premium for unlisted real estate.

• After standardising returns of unlisted asset classes for lagged reporting, listed and unlisted real estate are seen to be highly correlated to each other for Dutch funds (correlation of 88 percent), but less so for other Euro area funds and UK funds.

About the CEM data used in this study

Of the 20+ countries that provide data to CEM Benchmarking, only the subset of European funds is relevant towards understanding how European funds have invested in real estate. And while an even sampling across all of Europe would be ideal for this study, differences in culture and regulation of pension systems across countries motivate participation with CEM by some more than others.

Traditionally, funds from the Netherlands have seen the greatest participation with CEM, with funds from the UK seeing increasing participation. Other European countries that benchmark with CEM and are included in this study are funds from Denmark, Finland, the Republic of Ireland, Norway, Sweden, Switzerland and France. And while not all funds included in this study are traditional defined benefit (DB) pension funds, nearly all manage DB pension assets related to a DB pension liability; for the funds included for 2016, 92 percent are DB pension funds, 4 percent are buffer funds for DB pension systems, 3 percent are asset managers for DB pensions, and 1 percent are sovereign wealth funds.

Source:

1The eight aggregate asset classes included in the CEM Benchmarking study are: Public equity, private equity, fixed income, hedge funds, listed real estate, unlisted real estate, unlisted infrastructure and ‘other.’

You can download this article at: www.ipe.com/EPRA-IPERA-MayJune2019